How does an equity compensation package work

Understanding Types of Equity Compensation

Decisions: how to evaluate if you are getting a good offer

How to read your equity agreement

Using a portal: What to look for in the portal, how to exercise and sell

Liquidity Opportunities: IPO, Tender, Merger/Acquisition, Trading Windows

How do RSUs work?

RSU Tips

Understanding ESPPs: Benefits and Complexities

Understanding Non-Qualified Stock and Incentive Stock Options

NQSOs Taxes and Strategies

ISOs taxes and strategies

Building wealth through equity compensation and avoiding mistakes

How does an equity compensation package work

An employer’s compensation package typically includes salary, healthcare benefits, a retirement plan, such as a 401(k), and performance-based bonuses in some instances.

In the tech industry, receiving equity as part of your pay and compensation package is common. This means the company offers you partial ownership, usually through stock shares. However, equity compensation plans can vary significantly across companies, and these differences can influence how valuable they are to you, which we’ll explore in this guide.

Tech companies use equity compensation to encourage their employees to positively impact the company, which may increase the equity compensation value over time.

Almost all forms of equity compensation have a vesting schedule that creates an incentive or “golden handcuffs” for you to stay at the company and realize the value of your employer stock.

Vesting schedules usually have a time-based criterion. Exceptions include if a company is pre-IPO. In that case, a second triggering event is required, like an IPO, tender, merger, or acquisition.

Equity compensation can be a meaningful way to build your wealth over time. Depending on your equity type, the wealth-building opportunity will be different. For example:

- RSUs act as a function of your actual pay and count as W2 income.

- There are significant tax benefits in the case of ISOs and ESPPs

- You will have the ability to buy shares at a discount when dealing with ISOs, NQSOs, and ESPPs

Holding your shares once they have vested, been bought, or exercised and waiting for them to appreciate is a way to build wealth, but it has nothing to do with equity compensation itself.

It simply means that you are deciding to either not make any decisions or that you think this will be the best investment option available. Although this thinking can be reckless, it has minted many multi-millionaires. Managing this appreciated stock demands its articles and research. You can read more about that HERE.

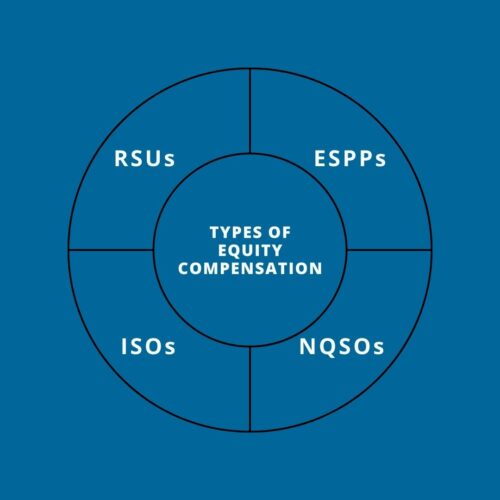

Understanding Types of Equity Compensation

There are four common types of equity:

- Restricted Stock Options (RSUs)

- Equity Stock Purchase Plans (ESPPs)

- Incentive Stock Options (ISOs)

- Non-Qualified Stock Options (NQSOs)

Other less common types of equity compensation include restricted stock awards or founder shares, performance units, and others.

The type of equity you get mostly depends on the life stage of your company and your role. For instance:

- Early-stage companies offer equity compensation in the form of ISOs, NQSOs, and founder shares

- As you get closer to an IPO, you may receive more RSUs

- Once the company has IPO’d, RSUs and ESPPs are most common

- Finally, if you are in a leadership position or a C-suite executive, it’s common to be compensated with ISOs, NQSOs, and performance units at all stages.

Most tech companies use a portal where you can access and manage your equity compensation. These include Shareworks, Carta, eTrade/Morgan Stanley, Fidelity, or Schwab. Each one will provide you with a login, allow you to see what kind of equity compensation you have, and allow you to make decisions, such as exercising and selling options.

Equity Compensation Packages: Key Terms, Concepts, and Decisions

The excitement of having an offer in hand can overshadow or entirely make you forget the offer details. However, making sense of your equity compensation package is critical to maximizing its potential.

Decisions: how to evaluate if you are getting a good offer

So, how do you know if you are getting a good offer? This depends on what stage of the company's lifecycle you are joining.

At an early-stage company, you are more likely to get equity instead of salary, bonus, or benefits such as a 401k. You will want to evaluate what percent of the company you are being offered.

As the company approaches a liquidity event like an IPO, you will want to evaluate your TC or total compensation. This can include your base salary, potential bonuses, and equity. Public data on roles and compensations become more available with later-stage and public companies.

At any stage, there are some resources available to help you make this critical decision:

- Teamblind.com: great peer resource, but be careful of biased answers

- Wellfound and Teamblind tools

- An attorney like Mary Russel from Stock Option Counsel

- Your local San Francisco Bay Area financial advisor

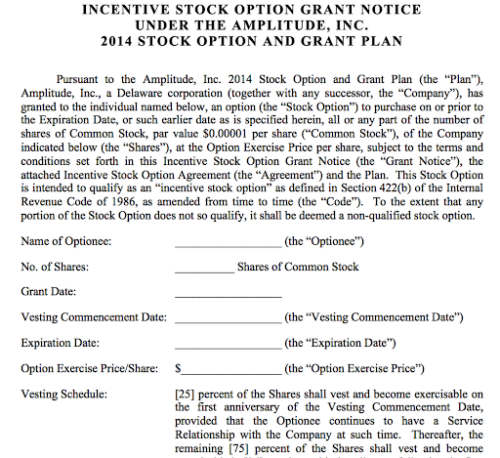

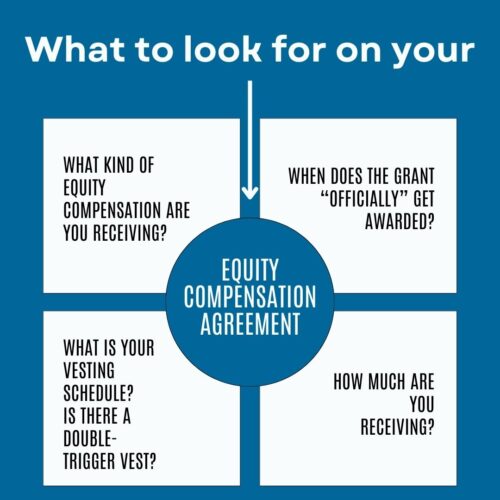

How to read your equity agreement

Don’t fret. Your equity compensation agreement may be very detailed and confusing if you are not familiar with this type of document. The good news is that only a few sections need your specific attention, as most of the document will include standard legalese.

Very often, the important sections are also displayed in your portal. Here’s what to be on the lookout for:

- What kind of equity compensation are you receiving? Each form of equity compensation usually has its award document. The type of equity you are being granted should be listed on the first few pages of the agreement.

- When does the grant “officially” get awarded? This doesn’t always coincide with your start date. The grant isn’t awarded until you sign off on the documents. Keep a close eye on this and ask for it to start sooner if the dates don’t look right.

- How much are you receiving? See how many shares or options you are receiving on the first few pages

- What is your vesting schedule? This will usually be explained in the document in written format rather than displayed in a table format. It should explain when the cliff occurs, usually one year from the start of the grant, and over what frequency and time frame the remainder of your equity will be given to you, aka vest. The cliff usually provides 25% of your grant and vests Contact us using this link if you need help with your equity compensation decisions.

- Is there a double-trigger vest? If you work at a pre-IPO company, you should look for the double trigger criteria. Usually, this states that a liquidity event is required for the equity to vest fully.

Depending upon the complexity of the agreement, you may want to hire an attorney specializing in equity compensation agreements. Here are some additional items to be aware of:

Depending upon the complexity of the agreement, you may want to hire an attorney specializing in equity compensation agreements. Here are some additional items to be aware of:

- Clawbacks: A legal clause that may force you to sell your shares back to the company or full forfeiture.

- Rights of First Refusal: Startups are staying private for a lot longer. You may want to sell your private shares. Some companies don’t allow this, or they will implement something called the right of first refusal.

- Double Trigger Acceleration Upon Change of Control: Think of this as a way to protect yourself from new management, so it may be worth exploring with your new employer if appropriate

Using a portal: What to look for in the portal, how to exercise and sell

Every portal will look slightly different. Companies like Carta and Shareworks tend to have more simplified portals than Schwab, Fidelity, or eTrade. It’s important to note that the latter are full-fledged brokerage firms with more technology and system features.

Regardless of the portal you use, you will be looking for the same four things in every portal:

- Type of equity. Your equity type is usually consolidated under one drop-down with all the relevant information below.

- Vesting schedule. The vesting schedule typically shows what has vested, what is waiting to be vested, and the dates.

- Exercise/Trade/etc. This will depend on who provides your portal, whether your company is public or private, and whether you can sell or take action.

- Tax Documents. This tab or part of the site will provide you with all the relevant tax documents you need to file your taxes.

Other parts of the portal can include a place to see your original grant documents, tools to run scenarios, portfolio summaries, and informational pages.

Liquidity Opportunities: IPO, Tender, Merger/Acquisition, Trading Windows

This is the moment every tech professional waits for the opportunity to sell and realize their riches. This moment comes at different times but always requires your equity to vest first.

IPO

The most monumental point in a startup's life is when it is finally ready for its IPO. There are two types of IPOs: traditional and direct listings.

A big bank usually underwrites traditional listings—think Goldman Sachs, Morgan Stanley, etc. Their job is to sell your employer's stock and get the best price possible. Because they are selling to big funds and other institutional investors, they need some enforcement to ensure the stock price doesn’t plummet on day one.

They do this using blackout windows, which are often six months long and during which you can not sell your shares. This creates a particularly big problem for those who may have to deal with RSUs vesting on the day of the IPO or those with ISOs that need to be sold to cover AMT tax bills.

A direct listing skips the underwriting process, and the company lists the stock directly on the stock market. With no promise of maintaining “price integrity” comes no blackout windows or lockup periods. Direct IPOs can allow employees to sell and act immediately.

Tender

A tender is an offer to buy a certain number of shares from employees, usually when the company is pre-IPO. Tenders usually occur when an investment firm wants to invest in the company outside of a traditional fundraising round.

Companies may use this as an opportunity to provide liquidity to their employees. Tenders will limit how many shares you can exercise/sell/etc. You’ll need to decide if you want to take advantage of this offer now or continue waiting for an IPO.

Merger/Acquisition

A merger or acquisition sometimes occurs instead of an IPO in the tech world. It can be a sign that things aren’t going quite well at creating expected value; other times, the strategic opportunity makes a lot of sense for both companies.

In any case, you should expect to receive some form of equity conversion. It could be cash for your stock, creating a taxable event, or a stock swap for the acquiring or merging company’s stock. Companies often honor your existing equity compensation grants, and your vesting schedule will be updated with the new company stock.

With that said, we’ve all heard horror stories, such as when Microsoft acquired Skype, leaving the employees with $0. That’s why clawback provisions are essential to identify and understand in your equity agreement.

Trading Windows

Once your company is publicly traded, you will likely be forced to follow trading windows. Trading windows prevent employees like you from trading based on insider information, especially before earnings are released.

Since earnings are released quarterly, you will have four yearly trading windows. During these times, you must make investment and trading decisions to ensure they are executed during the trading window. For instance, it’s important to understand how a decision that has tax ramifications may be impacted by trading windows.

Suppose you are a more senior employee or executive. In that case, you may be able to implement a 10b5-1, a preapproved and systematic sales process that provides a defense against allegations that sales are occurring based on insider information.

How do RSUs work?

What are Restricted Stock Units?

Restricted stock units (RSUs) are the most common form of equity received at a publicly traded tech company.

Although RSUs seem simple, a few components are critical to fully understand them so you can make intelligent decisions about your financial future.

RSUs are shares paid out to you throughout your vesting schedule. RSUs don’t require you to decide how and when you receive them. The key decision you will make is if and when to sell them.

When you are hired, you may receive an RSU grant. This grant will state how many shares are being paid to you and over what period. Think of RSUs as an extension of your salary and bonus.

To calculate the dollar amount of your RSU “compensation”, multiply the number of shares granted by the current market price. You will have some dollar price associated with the total shares. This is not the dollar amount you will receive. The amount you receive will depend on how the company shares perform throughout your vesting schedule.

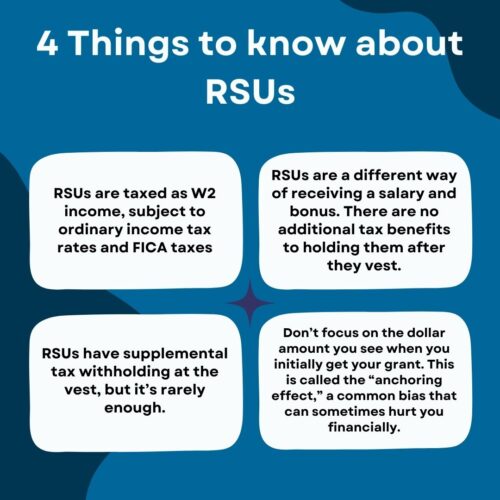

RSUs are taxed as W2 income, subject to ordinary income tax rates and FICA taxes. This can be seen as an extension of your salary and bonus. The dollar amount of this compensation is calculated by multiplying the number of shares vesting by the market price on the day of the vest.

Your company will be required to withhold some taxes at the vest. The federal withholding level is set at a fixed rate. If either 22% or your bonus and RSU come below $1,000,000, the typical withholding rate is 22%. If your RSUs/bonus is over $1,000,000, the withholding rate is 37%. Other taxes may also be applicable.

Depending upon your income level, it’s possible that as a highly compensated tech professional, the 22% rate may not be sufficient withholding for federal taxes. That’s why we highly recommend selling a few more shares when they vest and holding that cash in your bank account to cover any additional taxes that may be owed. Some companies allow you to adjust this withholding rate, but it is rare.

RSUs are also commonly used as a “refresh bonus,” so receiving additional grants during your annual performance review is common. Sometimes, these grants vest fully over just one year; other times, they follow the standard four-year vesting schedule.

RSU Tips

Because RSUs are the most common form of equity compensation, it’s fairly common for you to end up owning many company shares, which may cause an over-concentration. That’s why it’s important to fully grasp the ramifications of RSUs to ensure you are making informed decisions based on your financial and tax situation.

Here is a recap of tips related to RSU management:

- RSUs are a different way of receiving a salary and bonus. There are no additional tax benefits to holding them after they vest. If you hold them after they vest, buying your company shares is the best way to invest your additional salary and bonus. Ask yourself: “If I had the same amount of money but in cash, would I buy all these shares.”

- RSUs have supplemental withholding at the vest, but it’s rarely enough. The one thing that people hate more than paying taxes is being surprised by additional taxes. Consider selling some shares at the vest and putting the proceeds into your bank account.

- Don’t focus on the dollar amount you see when you initially get your grant. This is called the “anchoring effect,” a common bias that can sometimes hurt you financially. Remember that the dollar amount presented is only an estimate of how much you may expect to get. It’s not a promise, and it certainly is not a fair valuation of how much the company should be worth. This blog looks into other human biases and psychological traps you may want to avoid.

- To keep your tax bill at a minimum, consider selling RSUs in this order:

- Sell RSUs that you’ve held for quite some time and may have lost value

- Next, sell RSUs that are at break-even

- Lastly, sell RSUs where you have realized gains. You can read about RSU taxes HERE.

- If your RSUs vest during an IPO, you may have to wait six months before you sell them. During this time, the shares can drop. When you sell, you may need to sell extra shares to accommodate the higher price for the tax calculation.

Understanding ESPPs: Benefits and Complexities

An equity stock purchase plan (ESPP) is sometimes available to employees of publicly traded companies. ESPPs come in different formats, but traditionally, they allow employees to buy their employer's stock at a discount.

While an employer match to your 401k is optimal, the ability to participate in an ESPP is second best. It’s important to note that ESPPs can be a very complex form of equity compensation, even more so than ISOs.

Benefits of ESPP

The most common misconception about ESPP is that you may not want to participate because you are concerned about accumulating more of your employer's equity shares. However, the biggest benefit of ESPP is that it does not require you to hold the shares. It encourages you to sell your shares right away.

If your ESPP plan offers any form of discount, it doesn’t matter what the stock does; you will always make money. The only exception is if you are not in a trading window when the plan purchases the stock. This benefit is only amplified if you have a lookback provision. This provides you with a discount on either the lower of these prices:

- The offer period

- The day the plan makes the purchase

By selling the stock when it is purchased at a discount, net of taxes, you can sell and take that profit instantly, creating a risk-free return. For example, a 15% discount provides a return of 17.65%. Net of a hypothetical tax bill of 50% that is still a guaranteed 8.83% rate of return.

Here’s how the math works:

Let’s say you buy a $10 stock for $8.50. You then sell it for $10 for a $1.50 profit per share. By dividing the profit margin by the purchase price, the return is 17.65%. Then, assume that half the $1.50 profit will go toward taxes, your actual return is 8.83%.

Complexities of ESPPs

Similar to ISOs, ESPPs also have tax incentives associated with them if you hold them for some time. But be careful this is where things get complicated!

There is something called a “qualified disposition,” where you must hold the purchased shares for two years after the offer period and one year after the purchase. This changes some of the gains from ordinary income to long-term capital gains.

Not everything qualifies for the favorable long-term capital gains tax treatment, however. The rules around what gets taxed as ordinary income versus long-term capital gains are complex. We always advise you to keep your ESPP shares in the employer’s designated portal unless your tax advisor is highly confident in navigating the calculation and filing of the taxes. Additionally, selling may be more beneficial before reaching a qualified disposition in cases where the stock has lost value.

ESPPs contributions are capped at a maximum of $25,000 or 10% of your salary. With such “small” dollar amounts and big complexities for holding, we highly recommend you sell them, except in very special circumstances.

If you want to learn more about how ESPPs work, read our blog HERE.

Understanding Non-Qualified Stock and Incentive Stock Options

Stock options, another form of equity compensation, provide distinct benefits over RSUs or ESPPs. They offer flexibility, the ability to take advantage of timing, and tax benefits for ISOs. However, they are also complex, require more monitoring, and can come with severe tax consequences.

Like RSUs, stock options follow some form of vesting schedule. However, unlike ESPPs and RSUs, most stock options expire after ten years, requiring careful monitoring of your timeline.

There are two forms of stock options that you will commonly see: ISOs and NQSOs. The difference is in how taxes are handled. An easy way to remember: ISOs have preferential tax treatments while NQSOs don’t.

NQSOs Taxes and Strategies

NQSO taxes are straightforward and a good way to understand ISOs. When you exercise NQSO, the difference between the market or fair market value price and the exercise price is taxed as W2 income. There is usually some withholding, at around 22%, and you receive the net proceeds as shares. If you decide to hold the shares after the exercise, you will be subject to capital gains similar to if you were to buy any investment.

There are a few strategies to maximize NQSOs:

- Use leverage to your advantage: stock options provide leverage in time. You have time to see where the stock price goes before you commit any capital to the investment. This means your highest point of leverage is when the expiration date of the stock option(s) is furthest away. Use up that leverage/time to its fullest.

- Information Ratio: If you’re unsure when to exercise your NQSOs, consider the balance between their value and the time remaining. Financial professionals have tools to calculate this ratio and help determine the right time to exercise. However, a general rule of thumb is that the more “in the money” your options are, and the less time you have left, the more likely it’s a good idea to exercise—and the reverse is also true.

- Manage your tax bracket: Because NQSOs are considered W2 income, consider when and how much you exercise them. NQSOs can be used with deferred compensation or around an IPO when you may experience a large vest that creates a substantial tax event from your RSUs.

To learn about these strategies in detail and get additional tips, read our blog on stock options HERE.

ISOs taxes and strategies

ISOs come with a unique incentive from the IRS to encourage holding onto them. However, without considering these incentives, they function similarly to NQSOs. If you exercise and immediately sell the shares, the difference between the exercise and market prices will be taxed as ordinary income, a situation known as a disqualified disposition.

ISOs come with a unique incentive from the IRS to encourage holding onto them. However, without considering these incentives, they function similarly to NQSOs. If you exercise and immediately sell the shares, the difference between the exercise and market prices will be taxed as ordinary income, a situation known as a disqualified disposition.

A qualified disposition requires you to meet two holding periods:

- Two years from the grant date

- One year from the exercise date

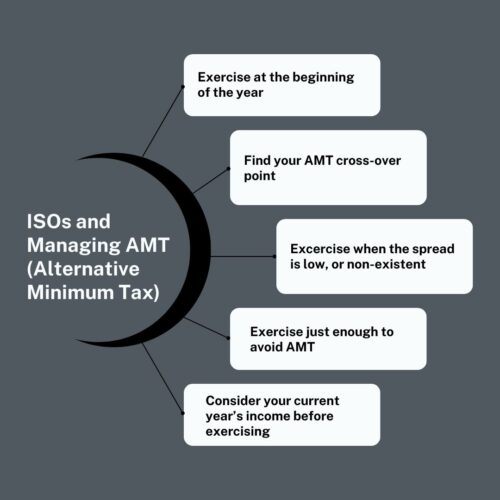

If both periods are met, the difference between the exercise and eventual sale prices will be taxed as long-term capital gains. Unfortunately, this comes with a very real trap called AMT.

When you exercise your ISOs, the difference between the strike and exercise prices will be considered a “preference item” for AMT. AMT is a parallel tax system; if there are “enough” preference items, it will kick in, and you will end up with a tax bill.

You could be hit with a significant tax bill if you’re a high-income individual with a large spread on your ISO exercise. Even worse, if you’re incentivized to hold your ISOs and the stock value drops, you may pay taxes on gains you never realized.

This happened to many tech employees during the 2001 tech crash, leaving some with enormous tax bills they couldn’t afford. This is why most ISO strategies focus on managing the Alternative Minimum Tax (AMT).

Here are two common approaches:

- Early Exercise: Many tech companies now allow you to exercise your options before they vest. The advantage is that the spread doesn’t exist yet, and you start the clock toward a qualified disposition earlier. However, if you leave the company before your shares vest, you must return the invested principal. This can be a substantial financial commitment, especially if you’re unsure whether your company will ever reach a liquidity event.

- Exercise Just Enough to Avoid AMT: Various tools can help estimate how much you can exercise without triggering AMT. Your financial advisor or tax professional can assist with these calculations. In some cases, running two parallel tax filings—such as in TurboTax—can help you pinpoint when AMT kicks in.

For more strategies on ISOs, read HERE.

Building wealth through equity compensation and avoiding mistakes

Over the past 15 years, we’ve seen tech professionals make and lose millions through company equity. The lure of striking it big is hard to resist, but balancing that potential with managing risk can be a real challenge.

Conventional wisdom in financial planning suggests that no more than 5% of your portfolio should be in a single stock. However, this can be tough to achieve in practice—whether because of your strong convictions about the stock or your role at the company.

Here are some of the employer stock tactics we deploy at RHS Financial:

- Defining Your Goals: How important are your goals? If you have goals like retirement coming up, you need to understand the impact that your employer stock can have on that goal. What happens if the stock drops by 50%? Can you still retire, buy that house, or afford that college education? If the answer is yes, then continue to hold. If the answer is no, you need to create a sales strategy.

- What is your risk tolerance? How old are you? Do you have your entire career in front of you? If so, you can make a mistake and gamble on your future. If you are getting closer to the end, every decision you make can make or break the rest of your life.

- Do you have assets outside of your employer's compensation? Can your other savings support your goals? If so, you can take this additional risk and opportunity.

- How sophisticated are you? Do you fully understand the risk you are facing? Have you been through market downturns? Do you understand market mechanics, risk, and rewards? If yes, then you may have what it takes to invest in something risky like your employer's stock.

- How bullish are you? Do you have strong confidence in the future of your employer's stock, or are you on the fence about what to do, so you elect to do nothing because you don’t know your alternatives?

As time passes and you experience success holding your employer’s stock, you may find yourself in a tough spot. You’re ready to sell your highly appreciated stock and know the risks, but the hefty tax bill is a major obstacle.

This is where understanding the tradeoffs between potential market drops, tax implications, creative strategies, and emotional factors can play a crucial role in protecting your gains. If you are in this situation, we strongly recommend consulting a San Francisco financial advisor who specializes in employer compensation tactics.

Finally, don’t discount the emotional baggage of managing your employer's compensation. Countless human biases are present including anchoring, regret aversion, loss aversion, overconfidence, and the endowment effect.

If you want to learn how to navigate these nagging feelings, then read our blog HERE.

If you need help with your equity compensation, contact one of our San Francisco Bay Area-based CERTIFIED FINANCIAL PLANNER™ Professionals. Use the link HERE to find a time on our calendar.